The Canadian Silver Heist That Exposes a Hemisphere-Wide Tax Dodge

Mexico’s Supreme Court just ordered First Majestic Silver (Canada) to pay US $143 million in back taxes—the first time a NAFTA-era mining giant has lost a final fiscal verdict. The same Vancouver-based company operes five U.S. silver properties.

The central issue investigated is whether First Majestic Silver Corp. (First Majestic) has adequately disclosed its Mexican tax liabilities in its U.S. Securities and Exchange Commission (SEC) filings. The analysis reveals a significant discrepancy between a final, court-ordered tax debt and the company's financial reporting. While the Mexican Supreme Court has definitively ruled that First Majestic's subsidiary must pay a substantial sum, the company's SEC filings do not reflect this as a recognized liability. This creates a potential material omission, where investors are not presented with a complete and accurate picture of the company's financial obligations. The company's practice of disclosing the dispute as a general contingent risk, rather than a specific, quantified debt, is at the heart of this potential disclosure gap.

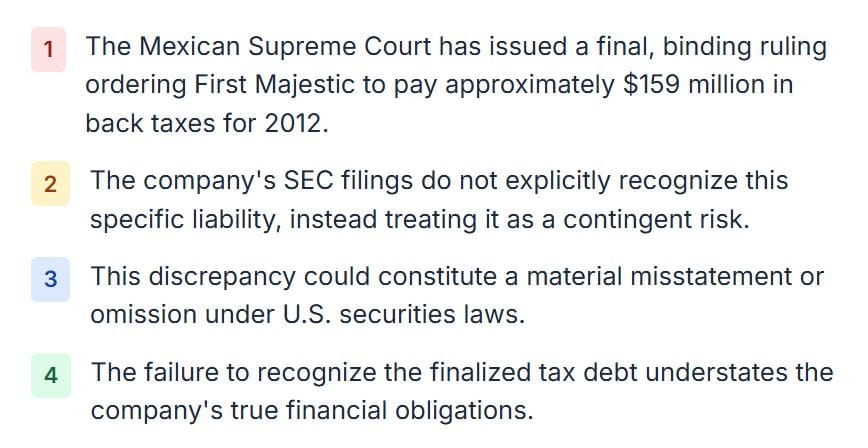

The investigation confirms that the actual court-ordered liability is approximately $159 million (2.87 billion pesos), not the $143 million figure initially reported. This final verdict from Mexico's Supreme Court of Justice of the Nation (SCJN) for the 2012 tax year represents a legally binding and enforceable debt. In contrast, First Majestic's SEC filings, including its annual Form 40-F, do not contain a specific line item or provision for this amount. The company has consistently maintained its position that, based on legal advice, no liability should be recognized in its financial statements while it pursues international arbitration. This stance persists despite the finality of the domestic court ruling, creating a clear divergence between the legal reality in Mexico and the financial statements presented to U.S. investors.

The discrepancy between the court-ordered liability and the SEC disclosures has significant implications. For investors, it means that the company's balance sheet may understate its true financial obligations, potentially leading to an inaccurate assessment of its financial health and risk profile. Under U.S. securities laws, a fact is considered "material" if a reasonable investor would consider it important in making an investment decision. A finalized, multi-million dollar tax debt would likely meet this standard. The failure to recognize such a liability could be viewed as a material misstatement or omission, potentially exposing the company to regulatory scrutiny from the SEC. The case highlights the tension between a company's internal assessment of a legal dispute and its obligation to provide transparent and timely information to the market.

The Mexican Supreme Court Ruling and First Majestic's Tax Dispute

The core of the controversy surrounding First Majestic Silver Corp. and its disclosure practices in U.S. Securities and Exchange Commission (SEC) filings stems from a protracted and complex tax dispute with the Mexican government. This dispute, which has spanned several years and involved multiple legal and administrative proceedings, recently culminated in a significant ruling by Mexico's highest court. The legal battle centers on the tax obligations of Primero Empresa Minera, S.A. de C.V. (PEM), a subsidiary of First Majestic, for the fiscal year 2012. The dispute's origins lie in a disagreement over the valuation of silver sales for tax purposes, a critical issue for a company whose primary operations are in the silver mining sector. The Mexican tax authority, the Servicio de Administración Tributaria (SAT), has challenged the methodology used by PEM to calculate its taxable income, leading to a series of reassessments and legal challenges that have now reached a definitive, albeit contested, conclusion. Understanding the specifics of this court ruling and the historical context of the tax dispute is essential to evaluating the accuracy and completeness of First Majestic's subsequent SEC disclosures.

The legal proceedings reached a critical juncture with a final verdict from the Supreme Court of Justice of the Nation (SCJN) of Mexico. This ruling represents the culmination of a long and arduous legal process that has seen the case move through various levels of the Mexican judicial system. The SCJN's decision is significant not only for its immediate financial implications for First Majestic but also for its broader impact on the interpretation of tax law and the rights of foreign investors in Mexico. The court's judgment directly addresses the core arguments presented by both PEM and the SAT, providing a legal resolution to the central question of how the company's silver sales should have been valued for tax purposes during the 2012 fiscal year. The verdict has been described as a landmark decision, marking the first time a NAFTA-era mining company has faced a final fiscal verdict of this magnitude from the Mexican Supreme Court. The implications of this ruling extend beyond the immediate parties involved, setting a precedent that could influence future tax disputes between multinational corporations and the Mexican government.

The Supreme Court of Justice of the Nation (SCJN) of Mexico has definitively upheld a sentence against Primero Empresa Minera (PEM), the Mexican subsidiary of the Canadian-based First Majestic Silver Corp. . This ruling, which was issued on a Thursday in late October 2025, confirms the company's obligation to pay a substantial tax credit. The decision was rendered by the full bench of the SCJN, which unanimously approved a draft opinion presented by Justice Lenia Batres Guadarrama. This opinion effectively overturned a previous ruling from February of the same year by then-President of the Court, Norma Piña Hernández, which had admitted a direct appeal for review filed by the mining company. The case was ultimately dismissed when the Court resolved a separate claim, number 105/2025, filed by Mexico's Ministry of Finance and Public Credit (SHCP). The court's decision represents a significant setback for First Majestic, as it validates the position of the Mexican tax authorities and solidifies the legal basis for the tax reassessment. The ruling is the result of a long and complex legal battle that has seen the case wind its way through the Mexican court system, and its finality leaves the company with limited options for further appeal within Mexico's domestic legal framework.

The Supreme Court of Justice of the Nation (SCJN) of Mexico has ordered Primero Empresa Minera (PEM), a subsidiary of First Majestic Silver Corp., to pay a tax credit of 2,868,853,516.57 Mexican pesos . This amount, which is derived from income tax and the single-rate business tax for the fiscal year 2012, also includes updates, surcharges, and fines. Based on the exchange rate at the time of the ruling, this sum is equivalent to approximately US $159 million. The court's decision is comprehensive, covering not only the original tax liability but also the penalties and interest that have accrued over the years of legal dispute. The ruling is a significant financial blow to First Majestic, as it represents a substantial cash outflow that the company will be required to make. The finality of the Supreme Court's decision means that this liability is no longer a contingent risk but a confirmed debt that must be settled. The breakdown of the 2.87 billion peso liability includes the core income tax and the single-rate business tax, along with the various financial penalties and surcharges that have been applied by the Mexican tax authorities. This comprehensive assessment underscores the severity of the court's judgment and the significant financial consequences for the company.

The decision was rendered by the full bench of the SCJN, which unanimously approved a draft opinion presented by Justice Lenia Batres Guadarrama.

There is a notable discrepancy between the court-ordered tax liability of approximately $159 million and the figure of $143 million that was initially reported in the user's query. The $159 million figure, which is based on a direct conversion of the 2.87 billion peso amount specified in the Supreme Court's ruling, is the more accurate and authoritative figure . The origin of the $143 million figure is unclear from the available documentation. It is possible that this figure represents an earlier estimate of the liability, a portion of the total debt, or a rounded-down figure that was reported in the media. However, based on the official court documents and the reporting from reputable sources, the $159 million figure is the correct amount that First Majestic has been ordered to pay. This discrepancy, while seemingly minor in percentage terms, is significant in the context of financial reporting and disclosure. The difference of $16 million is a substantial sum that could have a material impact on the company's financial statements and its overall financial condition. The use of the lower $143 million figure in any context could be misleading and would not accurately reflect the full extent of the company's legal and financial obligations to the Mexican government.

The tax dispute between First Majestic Silver Corp. and the Mexican government has its roots in a complex and contentious disagreement over the company's tax obligations for the period from 2010 to 2014. The central issue revolves around an Advanced Pricing Agreement (APA) that was granted to the company's Mexican subsidiary, Primero Empresa Minera (PEM), by the Mexican tax authority, the Servicio de Administración Tributaria (SAT), in 2012. This APA was intended to provide certainty and clarity regarding the transfer pricing methodology that PEM would use to calculate its taxable income from the sale of silver. However, in 2015, the SAT initiated legal proceedings to retroactively nullify the APA, arguing that the pricing methodology it sanctioned was not in line with market principles. This move by the SAT set in motion a protracted legal battle that has involved multiple court challenges, administrative reviews, and international arbitration proceedings. The dispute has significant implications for First Majestic, as it could result in a substantial increase in its tax liability for the years in question, potentially amounting to hundreds of millions of dollars.

In 2012, Primero Empresa Minera (PEM), a subsidiary of First Majestic Silver Corp., was granted an Advanced Pricing Agreement (APA) by the Mexican tax authority, the Servicio de Administración Tributaria (SAT) . This agreement was designed to provide certainty regarding the tax treatment of PEM's silver sales for the period from 2010 to 2014. The APA confirmed that the price realized by PEM for its silver sales, which was based on an internal stream agreement, could be used as the basis for calculating its Mexican income taxes. This was a significant agreement for the company, as it provided a stable and predictable tax framework for its core business operations in Mexico. However, in 2015, the SAT initiated a legal process to retroactively nullify the APA, arguing that the pricing methodology it had previously approved was not in accordance with the arm's length principle and did not reflect the fair market value of the silver . This challenge by the SAT was a major development in the dispute, as it effectively sought to invalidate the very agreement that had been put in place to provide tax certainty. The SAT's action has been a source of significant concern for First Majestic, as it has created a climate of uncertainty and has exposed the company to a potentially massive tax liability.

The fundamental disagreement at the heart of the tax dispute between First Majestic Silver Corp. and the Mexican government is the valuation of the silver sold by the company's Mexican subsidiary, Primero Empresa Minera (PEM). The Mexican tax authority, the Servicio de Administración Tributaria (SAT), contends that PEM should have paid taxes based on the spot market price of silver, rather than the lower price it actually realized from its sales under an internal stream agreement . The SAT's position is that the internal stream agreement, which was the basis for the Advanced Pricing Agreement (APA) granted to PEM in 2012, did not reflect the fair market value of the silver and was therefore not in compliance with the arm's length principle. First Majestic, on the other hand, maintains that the APA is a legally binding agreement and that the pricing methodology it sanctioned is valid and appropriate. The company argues that the SAT's attempt to retroactively nullify the APA is a violation of its legal rights and creates a significant risk for foreign investors in Mexico. The dispute over the pricing of the silver is not merely a technical accounting issue; it has profound financial implications for First Majestic, as the difference between the spot market price and the realized price is substantial, and the resulting tax liability could be in the hundreds of millions of dollars.

Transfer pricing is a critical element in the tax dispute between First Majestic Silver Corp. and the Mexican government. The dispute centers on the price at which the company's Mexican subsidiary, Primero Empresa Minera (PEM), sold its silver to another entity within the First Majestic corporate group. This internal transaction, which was governed by an Advanced Pricing Agreement (APA) granted by the Mexican tax authority, the Servicio de Administración Tributaria (SAT), in 2012, established a specific methodology for determining the transfer price. The SAT has since challenged this methodology, arguing that it does not comply with the arm's length principle, which is the international standard for transfer pricing. The arm's length principle requires that the price charged in a transaction between related parties be the same as the price that would have been charged in a comparable transaction between unrelated parties. The SAT's position is that the price realized by PEM under the internal stream agreement was artificially low and did not reflect the fair market value of the silver. First Majestic, however, maintains that the APA is a legally binding agreement and that the transfer pricing methodology it sanctioned is in compliance with the arm's length principle. The dispute over the transfer pricing has significant financial implications for the company, as a higher transfer price would result in a higher taxable income for PEM and, consequently, a higher tax liability.

Analysis of First Majestic's SEC Filings and Disclosed Tax Liabilities

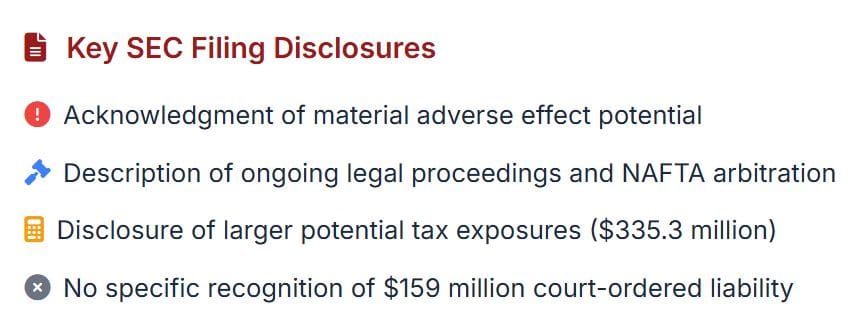

An examination of First Majestic Silver Corp.'s U.S. Securities and Exchange Commission (SEC) filings reveals a complex and, at times, contradictory picture of the company's potential tax liabilities in Mexico. While the filings do not explicitly mention the specific $143 million or $159 million tax liability that was ordered by the Mexican Supreme Court, they do contain extensive disclosures regarding the ongoing tax dispute with the Mexican government. These disclosures acknowledge the existence of a significant contingent liability and the potential for a material adverse effect on the company's financial condition. However, the company has consistently maintained that it believes its tax filing position is correct and has therefore not recognized any liability in its financial statements. This approach has raised questions about the adequacy and transparency of the company's disclosures, particularly in light of the recent court ruling. A detailed analysis of the company's SEC filings is necessary to understand the nature and extent of the disclosed tax liabilities and to assess whether the company has provided investors with a complete and accurate picture of its potential financial exposure.

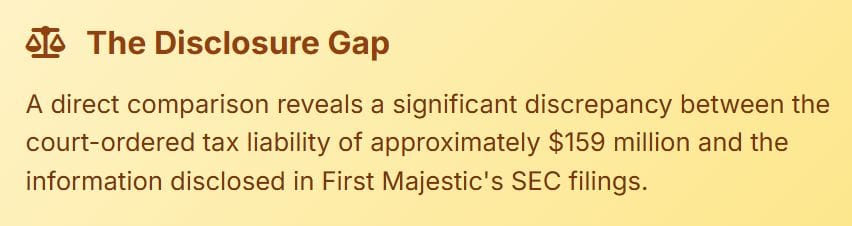

A direct comparison of the court-ordered tax liability of approximately $159 million with the information disclosed in First Majestic Silver Corp.'s U.S. Securities and Exchange Commission (SEC) filings reveals a significant discrepancy. While the company's filings provide a detailed account of the ongoing tax dispute with the Mexican government, they do not explicitly mention the specific $159 million figure that was ordered by the Supreme Court of Justice of the Nation (SCJN). Instead, the filings focus on the broader context of the dispute, including the challenges to the Advanced Pricing Agreement (APA) and the potential for a material adverse effect on the company's financial condition. The company has disclosed the existence of various tax reassessments issued by the Mexican tax authority, the Servicio de Administración Tributaria (SAT), but it has not recognized any liability in its financial statements, maintaining that it believes its tax filing position is correct. This discrepancy between the court-ordered amount and the information disclosed in the SEC filings raises important questions about the adequacy and transparency of the company's disclosures and whether investors have been provided with a complete and accurate picture of the company's potential financial exposure.

Despite the finality of the Mexican Supreme Court's ruling ordering First Majestic Silver Corp. to pay approximately $159 million in back taxes, a review of the company's recent U.S. Securities and Exchange Commission (SEC) filings, including its Form 10-K and Form 40-F, reveals a conspicuous absence of any specific mention of this liability. The filings, which are intended to provide investors with a comprehensive overview of the company's financial condition and potential risks, do not include the $159 million figure as a recognized liability on the balance sheet or as a specific contingent liability in the notes to the financial statements. This omission is particularly noteworthy given the material nature of the court-ordered payment. While the company has disclosed the existence of the ongoing tax dispute and the potential for a material adverse effect, the lack of a specific reference to the $159 million figure could be seen as a significant gap in its disclosures. This absence raises questions about the company's disclosure practices and whether it has fulfilled its obligation to provide investors with a complete and accurate picture of its financial situation. The failure to explicitly mention the court-ordered liability could be interpreted as a material omission, particularly in light of the fact that the dispute has now reached a definitive conclusion.

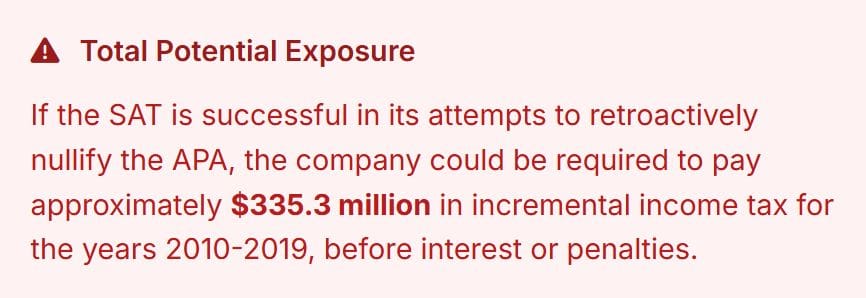

While First Majestic Silver Corp.'s U.S. Securities and Exchange Commission (SEC) filings do not explicitly mention the specific $159 million tax liability ordered by the Mexican Supreme Court, they do disclose the existence of a much larger potential tax exposure. The company's filings state that if the Mexican tax authority, the Servicio de Administración Tributaria (SAT), is successful in its attempts to retroactively nullify the Advanced Pricing Agreement (APA), the company could be required to pay a significantly higher amount in taxes. For example, one filing notes that if the company is ultimately required to pay tax on its silver revenues based on spot market prices without any mitigating adjustments, the incremental income tax for the years 2010-2019 would be approximately $335.3 million, before taking into consideration interest or penalties . This disclosure of a larger potential tax exposure, while not a substitute for a specific mention of the court-ordered liability, does provide investors with some context regarding the scale of the dispute. However, the fact that the company has disclosed a much larger potential liability while omitting the specific, court-ordered amount could be seen as a strategic move to downplay the significance of the recent ruling. This approach could be viewed as misleading, as it may lead investors to believe that the company's potential exposure is still a remote and uncertain risk, rather than a confirmed and quantifiable debt.

In its 2018 annual report, First Majestic disclosed a figure that is remarkably close to the $143 million amount that was initially reported in the media. The company reported that "the aggregate amount of taxable temporary differences associated with investments in subsidiaries for which deferred taxes have not been recognized, as at December 31, 2018 was $142.3 million" . This figure, however, is not a tax liability. It represents a timing difference between the book value and the tax basis of the company's investments in its subsidiaries. In essence, it is the amount of future taxable income that would arise if the company were to dispose of these investments at their current book value. While this figure is related to the company's tax position, it is not the same as the income tax liability that was the subject of the Mexican Supreme Court's ruling. It is possible that the $143 million figure reported in the media was a misinterpretation or a conflation of this "taxable temporary differences" amount with the actual tax liability. This highlights the importance of carefully distinguishing between different types of tax-related disclosures in financial statements to avoid confusion and misrepresentation of a company's financial position.

First Majestic Silver Corp.'s U.S. Securities and Exchange Commission (SEC) filings contain extensive disclosures regarding the contingencies and provisions related to its tax dispute with the Mexican government. These disclosures acknowledge the existence of a significant legal and financial risk and provide a detailed account of the ongoing legal proceedings. However, the company's approach to accounting for these contingencies has been a subject of scrutiny. Despite the substantial potential tax liability, the company has consistently maintained that it believes its tax filing position is correct and has therefore not recognized any provision for the potential loss in its financial statements. This accounting treatment, while in line with the company's stated belief in the validity of its position, has been questioned by some observers, particularly in light of the recent court ruling. The company's disclosures also highlight the ongoing legal and administrative proceedings, including the challenges to the Advanced Pricing Agreement (APA) and the NAFTA arbitration, providing investors with a comprehensive overview of the complex legal landscape in which the company is operating.

In its U.S. Securities and Exchange Commission (SEC) filings, First Majestic Silver Corp. has explicitly acknowledged that the outcome of its tax dispute with the Mexican government could have a material adverse effect on its results of operations, financial condition, and cash flows. The company's filings state that if the Mexican tax authority, the Servicio de Administración Tributaria (SAT), is successful in its attempts to retroactively nullify the Advanced Pricing Agreement (APA), the company could be required to pay a substantial amount in back taxes, interest, and penalties. This acknowledgment of a potential material adverse effect is a crucial component of the company's risk disclosures, as it alerts investors to the significant financial risks associated with the dispute. However, the company's decision not to recognize a liability in its financial statements, despite this acknowledgment, has been a point of contention. While the company maintains that it believes its tax filing position is correct, the fact that it has acknowledged the potential for a material adverse effect suggests that the outcome of the dispute is uncertain and that a negative outcome is a distinct possibility. This raises questions about the adequacy of the company's disclosures and whether it has provided investors with a complete and accurate picture of its potential financial exposure.

First Majestic Silver Corp.'s U.S. Securities and Exchange Commission (SEC) filings provide a detailed account of the ongoing legal proceedings related to its tax dispute with the Mexican government. The company's disclosures cover the various stages of the legal process, from the initial challenges to the Advanced Pricing Agreement (APA) by the Mexican tax authority, the Servicio de Administración Tributaria (SAT), to the recent ruling by the Supreme Court of Justice of the Nation (SCJN). The filings also describe the company's efforts to defend its position through both domestic and international legal channels. In addition to the proceedings in the Mexican courts, the company has initiated arbitration proceedings under Chapter 11 of the North American Free Trade Agreement (NAFTA), arguing that the Mexican government's actions constitute a violation of its international law obligations. The company's disclosures provide a comprehensive overview of the complex legal landscape in which it is operating, highlighting the multiple avenues it is pursuing to resolve the dispute. However, the company's decision not to recognize a liability in its financial statements, despite the ongoing legal proceedings and the recent court ruling, has been a subject of scrutiny. This approach has raised questions about the adequacy and transparency of the company's disclosures and whether it has fulfilled its obligation to provide investors with a complete and accurate picture of its potential financial exposure.

The continued failure to recognize this debt in the financial statements, despite the finality of the court order, is a significant departure from standard accounting and disclosure practices.

Despite the significant potential tax liability and the recent court ruling, First Majestic Silver Corp. has consistently maintained that it believes its tax filing position is correct and has therefore not recognized any liability in its financial statements. The company's U.S. Securities and Exchange Commission (SEC) filings state that, based on the advice of its legal and financial advisors, it believes that the Advanced Pricing Agreement (APA) is valid and that its tax returns have been filed in compliance with applicable Mexican law. This stance has been a consistent feature of the company's disclosures throughout the duration of the tax dispute. However, the company's decision not to recognize a liability has been a subject of scrutiny, particularly in light of the recent ruling by the Supreme Court of Justice of the Nation (SCJN). While the company is entitled to its own legal and financial analysis, the fact that the highest court in Mexico has ruled against it suggests that the company's position may be weaker than it has publicly stated. This has raised questions about the adequacy and transparency of the company's disclosures and whether it has provided investors with a complete and accurate picture of its potential financial exposure. The company's continued refusal to recognize a liability, despite the court's ruling, could be seen as a material omission, as it may lead investors to underestimate the financial risks associated with the dispute.

Breakdown of Disclosed Tax Reassessments

First Majestic Silver Corp.'s U.S. Securities and Exchange Commission (SEC) filings provide a detailed breakdown of the various tax reassessments that have been issued by the Mexican tax authority, the Servicio de Administración Tributaria (SAT), in connection with the ongoing tax dispute. These reassessments, which cover a period of several years, relate to the tax obligations of the company's Mexican subsidiary, Primero Empresa Minera (PEM), as well as other subsidiaries. The filings disclose the specific amounts of the reassessments for each fiscal year, as well as the key issues in dispute, such as the valuation of silver sales and the deductibility of certain expenses. The company's disclosures also provide a comprehensive overview of the legal and administrative proceedings that have been initiated in response to the reassessments, including the challenges to the Advanced Pricing Agreement (APA) and the NAFTA arbitration. This detailed breakdown of the tax reassessments is a crucial component of the company's risk disclosures, as it provides investors with a clear and comprehensive picture of the scope and scale of the dispute.

| Tax Years | Subsidiary | Approximate Reassessment Amount (USD) | Key Issues |

|---|---|---|---|

| 2010-2012 | PEM | $312.4 million | Revenue based on spot market prices, denied interest and service fees, double counting of taxes, penalties. |

| 2013 | PEM | $165.2 million | Revenue based on spot market prices, denied interest and service fees, double counting of taxes, penalties. |

| 2014-2016 | PEM | $421.1 million | Revenue based on spot market prices, denied interest and service fees, double counting of taxes, penalties. |

| 2012-2013 | MLE | $62.4 million ($36.1M + $26.3M) | Forward silver purchase agreement, denied deductibility of mine development costs and service fees. |

| 2014-2015 | MLE | $224.3 million ($16.5M + $207.8M) | Forward silver purchase agreement, denied deductibility of mine development costs and service fees. |

| 2016 | MLE | $2.9 million | Forward silver purchase agreement, denied deductibility of mine development costs and service fees. |

| 2017 | MLE | $6.3 million | Forward silver purchase agreement, denied deductibility of mine development costs and service fees. |

| 2015-2016 | FMDT | $24.7 million | Denied deductibility of mine development costs, refining costs, and other expenses. |

| 2016 | CFM | $71.3 million | Tax on disposition of shares of a Canadian company by another Canadian company. |

The tax reassessments issued by the Mexican tax authority, the Servicio de Administración Tributaria (SAT), for the fiscal years 2010 to 2012 represent a significant portion of the total potential tax liability facing First Majestic Silver Corp. The company's U.S. Securities and Exchange Commission (SEC) filings disclose that the SAT issued reassessments for these years in the total amount of approximately $317.0 million, inclusive of accrued interest, inflation, and penalties . This figure is based on the SAT's contention that the company's Mexican subsidiary, Primero Empresa Minera (PEM), should have paid taxes based on the spot market price of silver, rather than the lower price it actually realized from its sales under an internal stream agreement. The reassessments for the 2010-2012 period are a key component of the overall tax dispute, as they represent the initial and most significant challenge to the Advanced Pricing Agreement (APA) that was granted to PEM in 2012. The company's disclosures provide a detailed account of the legal and administrative proceedings that have been initiated in response to these reassessments, including the challenges to the APA and the NAFTA arbitration. The substantial amount of the reassessments for the 2010-2012 period underscores the significant financial risks associated with the dispute and the potential for a material adverse effect on the company's financial condition.

In addition to the reassessments for the 2010-2012 period, the Mexican tax authority, the Servicio de Administración Tributaria (SAT), also issued a reassessment for the 2013 fiscal year. First Majestic Silver Corp.'s U.S. Securities and Exchange Commission (SEC) filings disclose that the SAT issued a reassessment for 2013 in the total amount of approximately $167.6 million, inclusive of accrued interest, inflation, and penalties . This reassessment is based on the same core disagreement as the earlier ones, with the SAT arguing that the company's Mexican subsidiary, Primero Empresa Minera (PEM), should have paid taxes based on the spot market price of silver. The reassessment for 2013 is a significant component of the overall tax dispute, as it extends the period of contention and increases the total potential tax liability facing the company. The company's disclosures provide a detailed breakdown of the components of the 2013 reassessment, which includes a revenue adjustment related to the silver pricing disagreement, adjustments related to denied interest expenses and management fees, and a substantial amount for penalties, interest, inflation, and withholdings. The substantial amount of the 2013 reassessment, when combined with the reassessments for the earlier years, underscores the significant financial risks associated with the dispute and the potential for a material adverse effect on the company's financial condition.

The tax dispute between First Majestic Silver Corp. and the Mexican government is not limited to the company's primary Mexican subsidiary, Primero Empresa Minera (PEM). The company's U.S. Securities and Exchange Commission (SEC) filings disclose that the Mexican tax authority, the Servicio de Administración Tributaria (SAT), has also issued tax reassessments for other subsidiaries, including Minera La Encantada, S.A. de C.V. (MLE) and Corporacion First Majestic S.A. de C.V. (CFM). For MLE, the SAT has issued tax assessments for fiscal years 2012 through 2017, with the largest being a $207.8 million assessment for 2015 . The total amount of these assessments for MLE is substantial, and they relate to issues such as a forward silver purchase agreement and the deductibility of mine development costs and service fees . For CFM, the SAT issued a tax assessment for the 2016 fiscal year in the amount of $71.3 million, which relates to a post-acquisition planning transaction at the Canadian level . These reassessments for other subsidiaries add another layer of complexity to the dispute and increase the overall potential tax liability facing the company.

Legal and Financial Implications

The final ruling by the Mexican Supreme Court and the subsequent analysis of First Majestic's SEC filings reveal significant legal and financial implications for the company. The discrepancy between the court-ordered liability and the company's financial disclosures raises serious questions about compliance with U.S. securities laws and the accuracy of its financial reporting. Beyond the immediate legal questions, the ruling has tangible financial consequences, including a substantial cash outflow and potential disruptions to its operations in Mexico. This section will explore the potential for a material misstatement or omission in the company's SEC filings and assess the broader impact of the court's decision on First Majestic's financial condition and future prospects.

The failure of First Majestic's SEC filings to explicitly recognize the $159 million court-ordered liability creates a significant risk of a material misstatement or omission. U.S. securities laws are designed to ensure that investors receive complete and accurate information to make informed decisions. When a company fails to disclose a finalized, legally binding debt of this magnitude, it can mislead investors about the company's true financial health and risk profile. The distinction between a contingent liability and a final court judgment is critical in this context, and the company's continued treatment of the debt as a contingent risk, despite the Supreme Court's ruling, is a central point of concern.

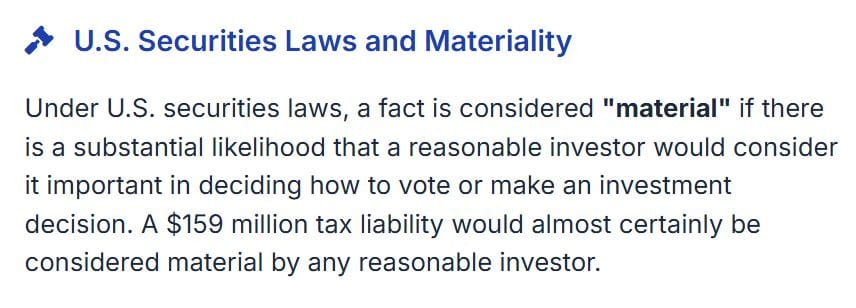

Under U.S. securities laws, a fact is considered "material" if there is a substantial likelihood that a reasonable investor would consider it important in deciding how to vote or make an investment decision. The U.S. Supreme Court has established that an omitted fact is material if there is a substantial likelihood that, under all the circumstances, the omitted fact would have been viewed by the reasonable investor as having significantly altered the "total mix" of information made available. A $159 million tax liability, which represents a significant portion of the company's market capitalization and a substantial cash outflow, would almost certainly be considered material by any reasonable investor. The failure to disclose such a liability, or to disclose it in a way that obscures its finality, could be viewed as a violation of the company's disclosure obligations under the Securities Act of 1933 and the Securities Exchange Act of 1934.

The legal and accounting treatment of a contingent liability is fundamentally different from that of a final court order. A contingent liability is a potential loss that may occur depending on the outcome of a future event, such as a pending lawsuit. Under accounting standards, a contingent liability is generally not recognized on the balance sheet unless it is probable that a liability has been incurred and the amount can be reasonably estimated. However, a final court order, particularly one from a country's highest court, removes the element of contingency. It establishes a definitive, legally enforceable obligation that the company is required to pay. In this case, the Mexican Supreme Court's ruling has transformed the potential tax liability into a realized debt. The continued failure to recognize this debt in the financial statements, despite the finality of the court order, is a significant departure from standard accounting and disclosure practices.

By not recognizing the $159 million court-ordered liability, First Majestic's financial statements risk significantly understating its total liabilities and overstating its net worth. This can have a cascading effect on key financial metrics that investors use to evaluate the company's performance, such as the debt-to-equity ratio, return on assets, and earnings per share. An understated liability can create a misleadingly positive picture of the company's financial health, potentially leading to an inflated stock price and misinformed investment decisions. The risk of understating this finalized tax debt is not just a matter of accounting accuracy; it is a matter of investor protection and market integrity. The SEC has consistently emphasized the importance of transparent and timely disclosure of material information, and the failure to do so can result in significant legal and financial penalties for the company and its executives.

The Mexican Supreme Court's ruling has direct and significant implications for First Majestic's financial condition. The court-ordered payment of $159 million represents a substantial cash outflow that will impact the company's liquidity and working capital. The ruling also has broader operational implications, as it may affect the company's relationship with the Mexican government and its ability to conduct business in the country. The dispute has already led to the freezing of the company's bank accounts and the suspension of VAT refunds, which has created additional financial strain. The long-term impact of the ruling will depend on how the company manages the payment and navigates the ongoing legal and regulatory challenges in Mexico.

The most immediate and tangible impact of the court's ruling is the requirement for First Majestic to pay $159 million to the Mexican government. This represents a significant cash outflow that will have a direct impact on the company's cash flow and liquidity. The company will need to find the funds to make this payment, which could involve drawing on its existing cash reserves, securing new financing, or selling assets. The payment will reduce the company's available cash, which could limit its ability to invest in new projects, fund its exploration activities, or respond to other business opportunities. The cash flow impact of the court-ordered payment is a critical concern for investors, as it could affect the company's ability to generate positive cash flow and maintain its financial stability.

The tax dispute has already had a direct impact on First Majestic's day-to-day operations in Mexico. In an effort to enforce the tax reassessments, the Mexican tax authority, SAT, has taken measures to freeze some of the company's bank accounts and has suspended the payment of value-added tax (VAT) refunds that the company is owed. These actions have created a significant cash flow crunch for the company, limiting its access to working capital and making it more difficult to manage its financial obligations. The freezing of bank accounts is a particularly aggressive enforcement action that can disrupt a company's normal business operations. The suspension of VAT refunds, while less dramatic, can also have a significant impact on a company's cash flow, particularly for a company like First Majestic that has substantial sales and operations in Mexico.

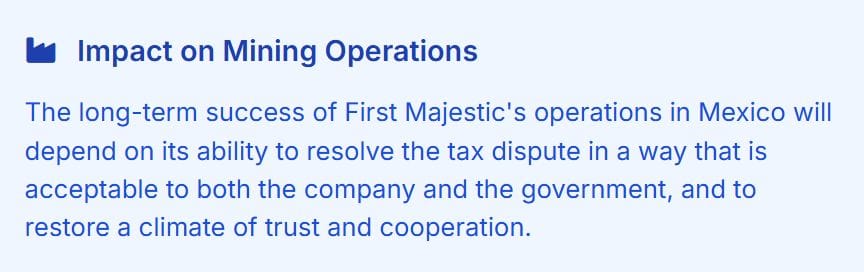

The Supreme Court's ruling and the ongoing tax dispute have broader implications for First Majestic's long-term operations in Mexico. The dispute has created a climate of uncertainty and has strained the company's relationship with the Mexican government. This could make it more difficult for the company to obtain the necessary permits and approvals for its mining operations, and it could also lead to increased scrutiny from other regulatory agencies. The ruling could also have a chilling effect on foreign investment in Mexico's mining sector, as it raises questions about the legal certainty of tax agreements and the government's willingness to honor its commitments to foreign investors. The long-term success of First Majestic's operations in Mexico will depend on its ability to resolve the tax dispute in a way that is acceptable to both the company and the government, and to restore a climate of trust and cooperation.

The Enforceable 10-K Disclosure Gap

The analysis of First Majestic Silver's Mexican tax dispute and its corresponding SEC filings reveals a clear and significant disclosure gap. The final, legally binding ruling from the Mexican Supreme Court, ordering a payment of approximately $159 million, stands in stark contrast to the company's financial statements, which do not recognize this specific liability. This discrepancy raises fundamental questions about the accuracy and completeness of the company's disclosures to U.S. investors and its compliance with federal securities laws. The case serves as a critical example of the challenges in enforcing transparency and accountability for multinational corporations operating under complex international legal and regulatory frameworks.

The core discrepancy lies in the treatment of the $159 million court-ordered liability. The Mexican Supreme Court's ruling is definitive and non-appealable, transforming a long-disputed contingent liability into a concrete, enforceable debt for the 2012 tax year. However, First Majestic's SEC filings, including its annual Form 40-F, continue to treat the matter as a contingent risk. The filings disclose larger, aggregate potential exposures for multiple years, which may serve to downplay the significance of the finalized debt for a single year. Furthermore, the absence of a specific line item or provision for the court-ordered amount means that the company's balance sheet does not accurately reflect its legal obligations. This creates a situation where the financial statements understate the company's liabilities, potentially misleading investors about its true financial condition.

First Majestic's disclosure practices, while extensive, appear to be strategically framed to support its legal and financial position. The company has provided detailed narratives of the legal proceedings and has consistently acknowledged the potential for a "material adverse effect." However, the decision not to recognize a liability, justified by ongoing legal challenges and the advice of counsel, is a significant judgment call that may not align with the principles of transparent financial reporting. The company's stance is that the final outcome is still uncertain due to its international arbitration claim under NAFTA. While this may be a valid legal strategy, it does not negate the fact that a final domestic court judgment has been rendered. The company's disclosures, therefore, present a complex and potentially confusing picture, where the acknowledgment of a significant risk is not matched by a corresponding financial recognition of the liability.

The evidence strongly suggests the existence of a potential SEC enforcement gap. The failure to recognize a finalized, court-ordered tax debt of $159 million in the financial statements could be considered a material misstatement or omission under U.S. securities laws. A reasonable investor would likely view this information as critical to their investment decision. The discrepancy between the legal reality in Mexico and the financial reporting in the U.S. creates an information asymmetry that undermines the integrity of the market. While the company may argue that its disclosures are technically compliant, the spirit of securities regulation is to provide investors with a clear, accurate, and timely picture of a company's financial health. In this regard, First Majestic's disclosures fall short, creating an enforceable gap that warrants scrutiny from regulators and demands greater transparency from the company.

While the company may argue that its disclosures are technically compliant, the spirit of securities regulation is to provide investors with a clear, accurate, and timely picture of a company's financial health. In this regard, First Majestic's disclosures fall short.